Italy, Coronabonds and a dilemma that wasn’t one

17 November, 2020

In a late-July post on PfEU, my colleague and fellow author Puneeth Parimisetty discussed the alleged dilemma that comes along with so-called “Coronabonds”, a debt instrument given out by the European Commission to counter the adverse economic effects of the COVID-19 pandemic in the European Union. The mutualization of sovereign debt in the EU has always been a highly contentious topic, and the current debate is no exception. The unusually high, almost American-style, degree of polarization that characterizes this debate has left dramatically little room for more moderate forces to maneuver and find a compromise.

It is undeniable that the severity with which the debate around a European solution for the ongoing coronavirus recession has been held has driven commentators from both sides to dig deep into their armories, giving birth to extravagant headers like “The European Hamiltonian Moment” or the almost ironic, self-dwelling coat of arms that reads “The Frugal Four”. As so often when emotions run high, the principle that “good policies are bad politics” reigns supreme and the mere prospect of a straightforward solution fuels the emergence of alternative facts.

In the case of Italy, most claims and accusations gravitate towards two different but similarly premature conclusions. First, that the notion of European solidarity has become nothing more than a bargaining chip for the country’s political elite—a group of individuals driven by inherently anti-European narratives that has deliberately wreaked havoc in a notoriously unstable political landscape only to promote their own political agenda. Second, that Italy’s inability to resort to fiscal countermeasures similar in size to those put in place by the economically more potent Germany ought to be blamed on the country’s “lack of fiscal discipline”, as my colleague writes, and that the high levels of public debt paired with anemic growth manifest an undisputed trajectory towards a new sovereign debt crisis. As with most myths, there lies a core of truth in these propositions, yet the grand scheme of things becomes visible only once the political fog of war is lifted.

Politics: The Resilience of the Center

The current coalition between the centre-left alliance, spearheaded by the social democrat Partito Democratico (PD), and the left-wing, self-declared anti-establishment party Movimento Cinque Stelle (M5S) came to be when the previous government fell apart in 2019. For a long time, M5S had campaigned with the promise never to enter a coalition with the “mainstream” social democrats. Yet, for two reasons the surprising alliance is likely to hold well into 2023. First, many first-row politicians of M5S are currently in their second term. Party statutes until very recently demanded politicians give up their posts after two legislative terms in order to limit the potential for political nepotism. Therefore, it is in many congressional representatives’ and senators’ interest for the coalition to last as long as possible. Second, the coalition is considered a firewall against the possibility of Matteo Salvini (Lega) becoming prime minister. Salvini’s party leads the current polls, indicating that a general election would likely result in a substantially different distribution of seats.

In 2022, the next President of the Republic will be elected for a term of seven years. Given that the current Italian President, Sergio Mattarella, has played an important role as an impartial mediator in the 2016, 2018 and 2019 political crises, it is of outmost importance to the parties of the middle (Forza Italia [FI], PD and M5S) to prevent the election of a more controversial candidate put forward by the right-wing Lega. The list of the more probable candidates includes former EU Commissioner and Prime Minister Mario Monti, as well as, according to some speculators, former European Central Bank (ECB) President Mario Draghi.

According to an advisor to the Government whose name shall remain undisclosed, while the coalition is unlikely to survive the next 12 months in its current form, there is the possibility for a new majority. About half the members of parliament from M5S are irritated by the current pro-European course of their party. The party became popular because it promised to return sovereignty to the Italian people in the aftermath of the European Debt Crisis, which is why the current European Solidarity Mechanism (ESM) debate has fueled a fire of anti-EU sentiment. The other half have adapted a more realist and practical approach to daily politics. Therefore, there is a real possibility that the party could split and partly fuse into an alliance with the PD, who in turn would enter a “grand coalition” with FI for a “Government of the Middle”. As much as Italian politics seems unstable and chaotic from a foreign point of view, there is a high chance that no anticipatory general election will be necessary.

The smoothness with which Italian politicians can jump over their ideological shadows is showcased by how parliament decided to vote on the Eurogroup’s three-pillar fiscal response to the pandemic’s impact on the economy. These pillars are an EIB guarantee fund, the SURE labor market program and ESM credit lines. While in favor of the first two pillars, M5S rejects the idea of calling on to the ESM once more, as such actions would diametrically oppose the notion of bringing back sovereignty to Italian people that fueled the party’s electoral campaigns in the past. It does not matter whether EU-policymakers ensure the Italian government that usage of ESM credit lines comes with very few strings attached; the way in which the country was treated in the aftermath of the European debt crisis permanently engraved the stigma of and sense of humiliation in utilizing any fiscal aide connected to the ESM. In order to overcome this legislative deadlock, M5S and the PD agreed on the following: Parliament would vote on a bill that included all three pillars of fiscal responses, therefore, making them available to the Government, in theory. In practice, the PD forwarded a political, though legally non-binding, declaration not to use ESM funds to support the Italian economy. Consequently, if M5S splits and a new grand coalition is formed in Rome, the realist wing of the party can together with PD and FI still apply for ESM funds, while the more radical wing of the party can claim to have fought against both a new application for an ESM program and the political mainstream.

The bottom line is that Italy’s political landscape might be notorious for its instability, but a better way in which to describe its topographic features might well be ever-changing. Centrist forces in the political system are surprisingly resilient and retain a pro-European bend, at times enabling them to act in a solution-oriented way unknown to most other European national parliaments.

Economics: The Frugal One

My colleague argues that “Southern countries desperately need financial reserves to maintain their spending sprees”. Indeed, it is true, the Italian public debt-to-GDP ratio had already been high before the onset of the COVID-19 pandemic, driven largely by legacy debts from the 1970s and 1980s and low growth since the introduction of the euro. During the Italian growth miracle of the 1950s and 1960s, Italy built up an extensive social welfare state similarly to other large European countries like Germany. However, even as growth petered out in the 1970s and 1980s, social welfare spending remained on an upward trajectory. As a result, Italy’s debt-to-GDP ratio ballooned.

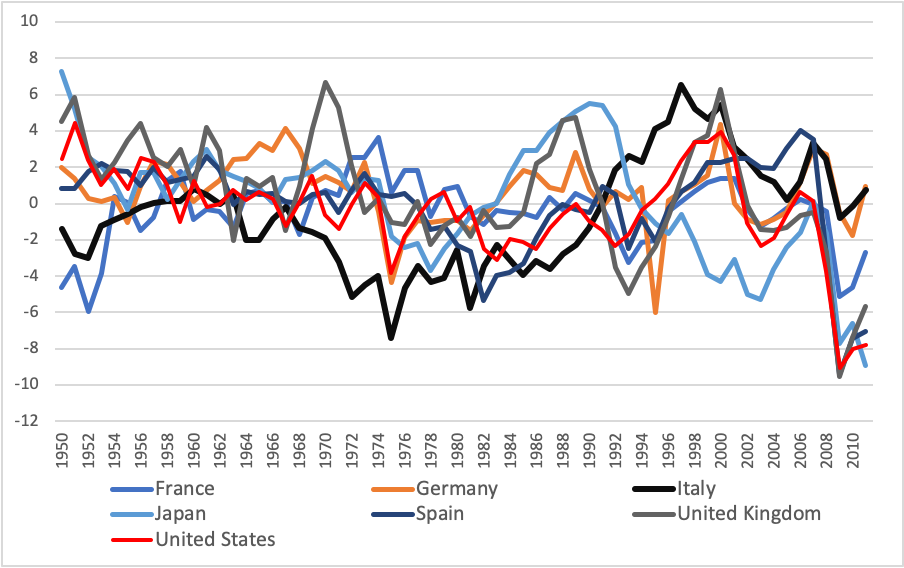

Though what most commentators fail to include in their analyses is the fact that, since the late 1980s, Italy has pursued relatively prudent fiscal policies (Chart 1). Measuring the government’s primary balance as a percentage of gross domestic product (GDP), we see how Italy went from being one of the worst performers to one of the best performers since the early 1990s when compared to other major advanced economies like Germany, France, the United Kingdom and Japan. Its debt-to-GDP ratio remained elevated, however, because of the overwhelming interest burden on the outstanding legacy debt, accompanied by persistently low growth.

Chart 1: Government primary balance as a percent of GDP

Source: International Monetary Fund (IMF), author’s own computations

It is no secret that the COVID-19 crisis will result in a further deterioration of Italian public finances as the Italian debt-to-GDP ratio is expected to increase from 134.8% at the end of 2019 to between 155-167% of GDP at the end of 2020. This would be more than twice the 77.2% of GDP currently projected for Germany. Due to the vast expansionary fiscal policies employed to support the economy, Italy’s overall balance is expected to drop to -12.7% of GDP in 2020, according to IMF projections. However, despite Italy’s high and increasing debt-to-GDP levels, there are three main reasons to believe that Italian debt can remain sustainable.

First, investor demand for Italian sovereign debt remains high on the back of a search for yield, home bias of domestic investors and central bank action. Issuance of new sovereign bonds have been consistently oversubscribed by investors for the past few months, indicating that demand far outstrips supply, despite sizable and frequent refinancing by the Italian government. The symmetric nature of the crisis seems to play an important role in driving investor demand. All EU27 economies have recorded steep rises in government spending to counter the economic impact of the crisis. Thus, Italy is not alone in this respect. There are three groups of Italian bond buyers underpinning demand: international investors, domestic investors and banks. For international investors, positive and slightly higher rates on Italian bonds vis-à-vis those of the nation’s European peers—many of which give negative yields for maturities up to 10 years or even beyond—make Italian sovereign paper relatively attractive. Consequently, Italian bonds comprise an important part of more risky but higher yielding bonds in these individuals’ euro area bond portfolios. Domestic investors and banks have tended to wade into the market whenever international bond holders have sold. Whilst this adds to the bank sovereign nexus, it stabilizes the bond markets in the short- to medium-term. The ECB’s monetary policy-driven purchase programs backstop further investor demand for Italian bonds. In a privately-held interview, the Italian economist Carlo Cottarelli, who was formerly the Director of the IMF’s Fiscal Affairs Department and the Extraordinary Commissioner for the Spending Review in Italy, pointed to the fact that while the Italian public accounts will suffer greatly from the economic crisis, most of the additional spending currently incurred is indirectly bought by the ECB in the secondary market. Therefore, unlike in the case of past surges in public debt, the current one does not increase Italy’s exposure to market movements, keeping investors speculating on the country’s default at bay.

Second, in contrast to my colleague’s classification of Italy as a “high-risk borrower with a high probability of default” and as a by-product of pronounced investor interest, interest rates on Italian sovereign paper are at historically low levels whilst spreads vis-à-vis the German bonds have narrowed considerably since mid-March (yields drop when prices of bonds rise). The spread on 10-year papers blew out to over 230 basis points versus German bonds in mid-March, as COVID-19 lockdowns unfolded across Europe and there was some doubt about the willingness of monetary and fiscal policymakers to step in. But the March announcement of the 750 billion ECB Pandemic Emergency Purchase Programme (PEPP) stabilized expectations in bond markets and drove down the spread by over 50 basis points. The April 500 billion Eurogroup loans package and the July European Council agreement on a 750 billion recovery package for post-2021, of which Italy will be one of the main beneficiaries, have narrowed spreads further to about 150 basis points—a level similar to the pre-COVID-19 era.

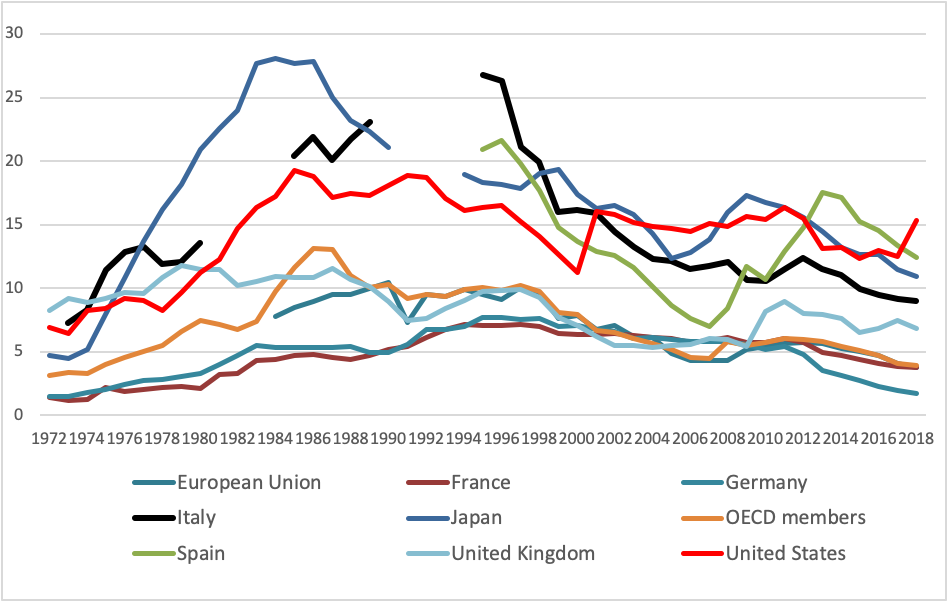

Third, and presumably underlying investor confidence in Italian sovereign debt, Italian interest payments as a percentage of government revenues remains relatively low. The debt-to-GDP ratio is only one metric to look at debt sustainability. An alternative metric is the interest payments as a percentage of government revenue. This metric is arguably better because it measures the refinancing cost of a government as a share of its income, i.e. government revenues. As can be discerned in Chart 2, the Italian interest burden has been on a steep declining path for over 20 years and is now below the level of the United States.

Chart 2: Interest payments as a percent of government revenues

Source: International Monetary Fund, author’s own computations.

Naturally, a residual risk always remains, mainly in the form of a potential rollover crisis. Whilst interest burdens are manageable and have been contained by the actions of the ECB and the EU, investors may at some point lose faith in the ability of the Italian government to pay back the principal on the sovereign debt. The support from SURE, the Next Generation EU funds and the ECB make this unlikely in the near run. Yet, in the long run, particularly if Italian growth remains as tepid as its politics combustible, such a scenario must never be fully excluded.

A possible trigger for a sell-off in Italian bonds could be continued low growth. If investors lose faith in the underlying earnings capacity of the Italian economy, they may see repayment of the principal amounts as no longer viable, even if Italy can still carry its interest burden. At 160% of GDP, the outstanding stock of debt will be sizable and could spiral out of control if growth continues to disappoint on the downside through denominator effects.

An increase in inflation could also become a possible trigger for a sell-off in Italian sovereign paper. Inflation is below targets in two-thirds of inflation-targeting countries. Since the onset of the pandemic and the sharp fall in commodity prices—crude oil in particular—inflation and inflation expectations have registered further declines in many economies. Despite increases in monetary aggregates on the back of central bank action, inflation remains below the ECB’s target of close to but below 2%. Some, like Carlo Cottarelli, fear that inflation tends to be “unleashed” once a certain threshold is passed, and higher inflation could lower demand for low interest rate bonds. Moreover, if inflation were to increase sharply, the ECB would have to mop up excess liquidity by selling government bonds, including those with high spreads with respect to German bonds—like Hellenic or Italian titles—thus adding further pressure on the bond market. “The real danger”, Cottarelli concludes, “will come when the ECB has to reverse the current purchasing program. This moment will not come today, and not tomorrow. But it will come.”

Conclusion: A Leap of Faith

Due to its high public debt level, anemic growth and volatile politics, Italy has since long been perceived as the cardinal risk to the stability of the Eurozone. By the stroke of ill fortune, Italy happened to be the first European country affected by an escalation of the novel coronavirus. There can also be no doubt that the Italian economy suffers from myriad structural weaknesses, which are likely to be compounded by the ongoing coronavirus recession. These include, above all, persistently low growth rates, decreasing competitiveness and an entrenched North-South divergence that all feed into the high debt-to-GDP ratio.

However, this by no means implies that a sovereign debt crisis, euro-exit or overall demise of Italy is the logical conclusion, as is often presupposed in other parts of Europe. Italy has a number of strengths: Centrist forces in its political system are surprisingly resilient and retain a pro-European bend, Italy had run a primary fiscal surplus for over 30 years and its Northern regions continue to be home to a strong industrial base as evidenced by Italy’s consistent export surplus. Moreover, Italy boasts limited household debt, in particular as opposed to other European countries.

From a European perspective, the key question will be how to aid Italy in a process of modernization and reform. The central tension is between imposing conditionality from Brussels or providing the funds with a generosity that puts the responsibility solely on the shoulders of national Italian policymakers. So far, the EU has managed to pave the way for Italian policymakers to avoid a political backlash and take up EU support to stabilize the economy. In fact, Italy has received the highest proportion of grants from the Next Generation EU (NGEU) recovery package and SURE unemployment insurance loans. Yet, letting go of conditionality is a leap of faith for the Union, the rewards of which will only materialize if met by a genuine Italian modernization drive.