Coronabonds - A European Dilemma

29 July, 2020

The collapse of Iceland’s banking system began the European sovereign debt crisis of 2008, which peaked in 2010 and continued till late 2012. This crisis caused significant political turmoil and an enormous economic recession within the European Union. The eurozone crisis of 2008 also initiated the debate on the issuance of bonds without borders called “Eurobonds”. Despite many attempts by a few members states, the bid for Eurobonds never saw the light of day. Almost a decade later the broadly felt impact of the global COVID-19 pandemic—which has crippled many European economies—has led to the reemergence of the Eurobonds debate. Now called coronabonds, this economic mechanism has created a divide and animosity within the time-tested union.

What are coronabonds, and how do they work?

Coronabonds are bonds without borders, which means all the member states of the European Union will issue a joint debt creating an EU-wide mutualised debt. The communisation of debt will result in a higher probability (p) of repayment and, reduces the lender’s costs (1+r), on which interest rates are primarily calculated.

P (probability of repayment) x (1+rL) (lender’s revenue if repaid) = (1+r) (lender’s costs)

A battle of Austerity vs. Spending, Rich vs. Poor, North vs. South

Currently, 9 EU member states including Italy, Spain, and France are urging for mutual issuance of debt in the form of coronabonds. One striking similarity between these member states is that they are categorised as high-risk borrowers with a high probability of default; hence they are obliged to pay a high-interest premium on their borrowings. In opposition to corona bonds are the frugal four — Austria, Denmark, Sweden and the Netherlands, with Finland being the newest member to oppose the corona bonds. Widely termed as fiscally conservative, these low-risk countries have a low probability of default and, therefore, end up paying a low-interest premium on their borrowings. It is indisputable that a joint issuance of EU wide bonds will lower the probability of default, pulling down the interest rates for the member states in favour of coronabonds. However, it also means higher interest rates for a few financially well-performing countries like the Netherlands.

With the country’s death toll surpassing 34,000 and the economy in a slump, the global COVID-19 pandemic has paralysed the Italian economic machine. This economic crisis has brought mounting political pressure on the current Italian prime minister, Giuseppe Conte, to revive the economy. At the heart of the coronabonds debate is the notion of European solidarity in times of crises like these. Southern European countries like Italy contend that they have suffered the most during this pandemic and unlike the 2012 debt crisis, this was most certainly not their fault. Italy and Spain also argue that other European member states watched their struggle and built their response system to the virus from their mistakes and examples. Italy cites that the EU often speaks of European solidarity, shared history, and ideals. If the notion of European solidarity is not applicable now during an unprecedented global pandemic, it is hard for Italian voters to imagine a possible circumstance when it would be.

In opposition to these views, the German chancellor, Angela Merkel has initially dismissed any scope of corona bonds becoming a reality, making Germany the “Bond villain.” But in a twist of events, the German chancellor, Angela Merkel has made the biggest U-turn in her political career highlighting a crippling dilemma within the European union.

The frugal four perceives corona bonds as a problematic political affair that is unnecessary and dangerous. The frugal four argue that coronabonds do not represent solidarity, but rather serve as an instrument that rewards the years of financial mismanagement and lack of fiscal discipline of a few member states. The coronabonds will push Europe into crisis by dragging countries with good credit ratings, into immense debt. All participating states would not only have to undertake an indefinite financial liability in the event of a default by weaker states but would also have to repay a substantial part of the mutualised debt with their own tax-payers money, incurring substantial political costs in the process. The high levels of debt in the Southern European countries do not correlate with the COVID-19 pandemic. For instance, France spends considerably more on maintaining the public infrastructure than Germany and accepts a higher public debt. In unprecedented times like these, the southern countries desperately need financial reserves to maintain their spending sprees and are using this pandemic as a means to justify their lack of fiscal discipline.

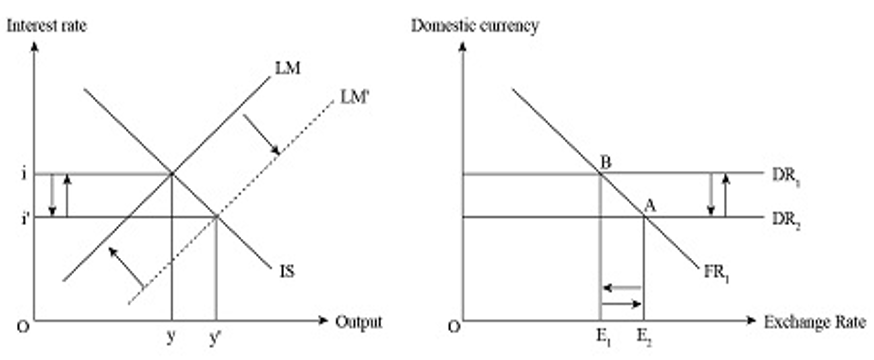

Potential risks of coronabonds (IS-LM-FX model)

Figure: IS-LM-FX interaction model

Not only is the issuance of mutual debt bonds like corona bonds financial disadvantageous for the frugal four, but there is also a prevalent contention that such measures would result in the loss of financial control. In most European countries, the elected parliament has influence and control over government spending (IS curve). Many well performing states like the Netherlands would lose this autonomy of control with the issuance of mutual debt, as it transcends the realm of influence of the existing democratic architecture. It would take an interminable time before coronabonds could fit into national and the overall European economic and legal systems. This is a dubious effort, especially in these unprecedented times and considerable economic tensions. There is a risk that the southern European countries could use coronabonds and their legal anchoring as a gateway for establishing permanent Eurobonds.

The issuance of coronabonds for an indefinite period of time will lead to abuse and exploitation in the long run by a few member states as they deviate from their national responsibilities for their debt. Currently, there are no sanctions for defaulting members states, and the pooling of debt via coronabonds will make it even harder to penalize fiscal irresponsibility moving forward. This will result in northern states financing (via taxpayers’ money) the debts of the southern states but without having any command on the economic policies of these nations. An alternative to issuing coronabonds would be to initiate EU-wide standard economic and financial policies. This would mean, however, that states would lose their autonomy on government spending (IS curve) and undertake substantial political costs—concessions they seem highly unlikely to make.

There is also a potential threat that coronabonds might increase interest rates overall in the long run, a complete opposite of the intended result. Most countries within the European monetary union (EMU) do not have monetary autonomy (fixed LM curve) as they follow a fixed exchange rate and either peg their currencies against the Euro or have a single currency Euro. With the issuance of mutual debt, these countries would also lose their fiscal autonomy (IS curve) and, consequently, all control over the interest rates and forex market (FX market). In the case of substantial financial mismanagement and unrestricted sovereign default, this situation will push the entirety of Europe into an irrevocable economic crisis. Therefore, coronabonds do not seem to be a viable instrument to tackle the coronavirus crisis and are very risky in extraordinary times like these.

Concluding remarks

In summary, coronabonds have been used as a political instrument by a few right-wing politicians like Matteo Salvini and Giorgia Meloni to not only escape the blame for their lapses in dealing with the pandemic but push it onto northern states to promote their political agendas. Issuing coronabonds in the name of European solidarity will only initiate a new sovereign debt crisis in Europe, incapacitating the European economy in the long run. European solidarity and harmony have, nonetheless, prevailed during this crisis in their own special ways. Germany treating COVID-19 patients from northern Italy and France is a testament to the commitment of European values and solidarity. The EU Council has recently agreed on issuing bonds with maturities of 3 to 30 years to allot a 750 billion euro recovery fund, as a coronavirus stimulus package based on common borrowing. More than half of the funding (390 billion) is to be allotted as grants, and 360 billion in loans ensuring individual liability of the member states. The issuance of loans will also mandates the member states to compile with the conditions of usage of these funds for country-specific recommendations by the EU and to follow the principles of good governance to prepare national recovery and resilience plans for 2021-2023. Even though the recovery fund does not exactly function like corona bonds, it is a massive step towards the creation of a more robust European project without comprising economic stability and ensuring accountability with in the member states of the union.