The Division of Europe: Mistrust and Macroeconomic Myths

How the Frugal Four weaponize the narrative of fiscal irresponsibility to oppose debt mutualization

7 September, 2020

After months of tension and four days of intensive negotiations, the EU Member States came to a deal on the multiannual financial framework (MFF), and a coronavirus recovery package. The conflict centered around one of the most contentious questions in Europe: could the European Monetary Union be joined by a public debt union?

These negotiations have taken place during extraordinary levels of post-war government spending as states try to respond to the economic impact of the pandemic. Most EU Member States are now running deficits above the 3% of GDP public spending cap imposed by the suspended Growth and Stability Pact.

During negotiations, a clear division emerged, with Southern Member States calling for greater pan-European solidarity while some Northern neighbours, the so-called frugal four, have dug their heels in the sand.

In practical terms, solidarity means spending, and Southern Member States have proposed that a common European institution issue joint debt to finance each member state’s crisis response. This proposal became popularized and hotly debated under the name of ‘coronabonds’.[i]

The conflict is not merely a question of economics, but also of politics. Various proposals to fund Europe’s economic recovery were put forth over the course of negotiations. But to focus on the conflict over the terms—whether grants take precedence over loans, the measurement for funding allocation, or the extent of supervision—obscures the underlying debate over responsibility and trust between Member States. The core difference in the proposals is their differing interpretations of European solidarity and the macroeconomic imbalances across the EU.

Proposals and Fault lines

The discussion on European fiscal integration was spurred on by Italian Prime Minister Giuseppe Conte. Rather than settle for using the European Stability Mechanism for fiscal support, eight euro area governments, including France, Spain, Portugal, and Greece, jointly signed a letter in late March calling on the President of the European Council, Charles Michel, to “work on a common debt instrument issued by a European Institution to raise funds on the market.” The signatories put forth a clear appeal to European solidarity, citing the severe economic damage they have suffered as a result of the pandemic.

The following days of negotiations quickly devolved into a North-South conflict, reaching its climax when Portuguese Prime Minister António Costa called Dutch Finance Minister Wopke Hoekstra ‘repugnant’. His outrage, echoed by Spanish and Italian government officials, came as a response to Hoekstra’s questioning as to why some states were unable to finance their own recovery. To the Southern alliance, this line of questioning was dangerously reminiscent of the eurozone crisis when stringent criteria and painful reforms were the price Member States had to pay for bailout packages.

This time around, Southern government leaders emphasized that their economies have matured. “It is not as if Spain has not been doing its homework,” said Foreign Minister Cristina Gallardo, “We’ve been reducing our public debt, we’ve been reducing our deficit, we’ve been reforming our retirement age.”

Surprisingly, they have found allies in unexpected places—the German government. In an open letter in early April, German Foreign Minister Maas and Finance Minister Scholz maintained that, “the Member States have varying financial capabilities with which to respond to this economic crisis, for which nobody is to blame.” This departure from Germany’s European policy orthodoxy was followed up by the Franco-German proposal, which had the European Commission raising $500bn euros in loans and then distributing grants to Member States.

The Franco-German proposal was opposed by Austria, the Netherlands, Denmark, and Sweden, who have become known as the ‘Frugal Four’. Their counterproposal called for loans instead of grants, reiterated their strong opposition to any form of debt mutualization and demanded “a strong commitment to reforms and the fiscal framework.” The aim, in their own words, is to ensure that “all Member States are better prepared for the next crisis.”

In their attempt at bridge building, the European Commission put forth a new proposal, ‘Next Generation EU’, centered around an enormous investment program of €750bn in grants and loans to Member States and European recovery priorities. During the marathon negotiations on the weekend of the 17th of July, the sides retreated to their trenches. The Southern states made their case for recovery support in the form of grants, the frugal four insisted on loans and conditionality, and Merkel, Macron, and Michel worked to find the golden mean.

The rhetoric was emblematic of the conflicting narratives at the root of this debate. Before entering the negotiations, a pessimistic Dutch Prime Minister Rutte told the Dutch media that although he was in favour of solidarity “from countries that can now make some more room in their budget to fight the crisis, towards countries that cannot,” such solidarity should come with “the request to those countries to do everything in their power to be able to solve it by themselves next time around. And that means reforms, in the labour market, in the pensions….”

Testing the Narrative of Fiscal Irresponsibility

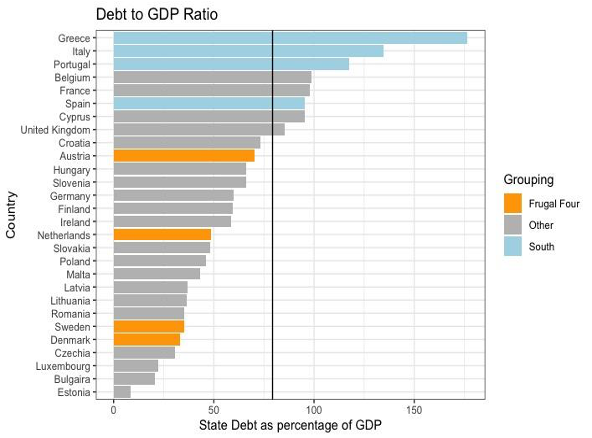

The deeply conflicting position of each bloc is rooted in mistrust and macroeconomic myths. The Frugal Four, on the one hand, point to the high public debt that the Southern countries have accumulated to support arguments that these governments must rein in their spending and reform their economies to encourage growth. The Southern Four’s pledge for solidarity, on the other hand, stresses the blameless exogenous shock of coronavirus as the cause of their steep economic decline. Greece, Italy, and Spain, for example, are all forecasted to see their economies shrink by nearly 10%.

The deeply conflicting position of each bloc is rooted in mistrust and macroeconomic myths. The Frugal Four, on the one hand, point to the high public debt that the Southern countries have accumulated to support arguments that these governments must rein in their spending and reform their economies to encourage growth. The Southern Four’s pledge for solidarity, on the other hand, stresses the blameless exogenous shock of coronavirus as the cause of their steep economic decline. Greece, Italy, and Spain, for example, are all forecasted to see their economies shrink by nearly 10%.

This appeal for solidarity has been undermined by a dominant narrative that Southern-European workers are their economies are macroeconomically unsound, and their governments are fiscally irresponsible, as exemplified in statements by Northern policymakers. In this light, unconditional loans and shared debt become a dangerous and the prosperous northern countries become the “Fiscal Responsibility Police” demanding reforms and strict monitoring in return for loans financed by their taxpayers. Moreover, the myth of fiscal irresponsibility becomes the foundational myth dividing Northern and Southern Europe.

However pervasive, this myth often remains implicit and, consequently, unchallenged. The data are much less damning than the myth would suggest: the statutory retirement age in Greece is higher than that in the Netherlands, the Frugal Four relatively spend more on social policies than their Southern neighbours, and Southern workers annually work hundreds of hours more than their Northern counterparts.

Broadly, northern skepticism can be divided into labour market criticisms and public finance criticisms. The trope of the “lazy” Southern worker is addressed by examining data on working hours and retirement ages. The references to macroeconomic vulnerability are investigated through public spending statistics, primary deficit calculations, and data on the cost of borrowing by Member States. The results of these examinations force reflection on the need for revenue rather than spending reforms and the structural conflict at the heart of the eurozone’s interest rate divergence, which could leave some economies perpetually underinvested.

The Labour Market Critique

The myth of fiscal responsibility is often paired with a perceived difference in work ethic. In Dutch media, for example, the May cover of a major center-right magazine declared ‘not another penny to Southern Europe’ accompanied by caricatures of hard-working, blonde northerners juxtaposed with sunbathing, wine-drinking southerners. When looking at the numbers, however, the common trope of the less laborious Southern European appears unfounded. Workers in Southern Europe spend less time on the beach and taking siestas than their Northern neighbors lead us to believe.

Working Hours

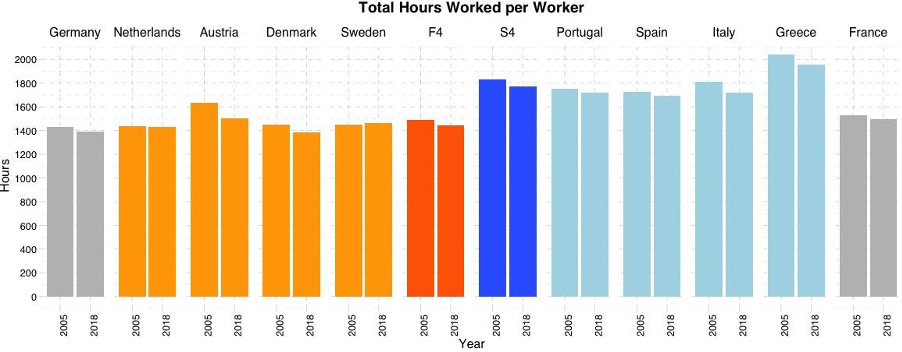

According to data from the Organization for Economic Cooperation and Development (OECD), workers in every southern economy actually work longer hours than their frugal counterparts. This is true when measuring total hours worked annually and weekly hours worked by only full-time employees (excluding Austria).

Annually, Southern European workers spend an average of over three hundred hours more at work than workers in the Frugal Four countries. In 2018, the average Greek worker worked close to 2000 hours, while the Danish, German and Dutch worked the least out of all EU Member States at only 1382, 1390, and 1431 hours per year, respectively. The average full-time employee in the European South, had a longer work week by 2 hours in 2005 and 2.5 hours in 2018 as compared to a full-time worker in the European North. Although this may not seem like much, it amounts to an extra working day every single month. When factoring in part-time work, the regional difference in hours worked grows for German and Dutch workers. To imply that the Southern economies would fare better if they were as laborious as their Northern counterparts is, therefore, unfounded.

Annually, Southern European workers spend an average of over three hundred hours more at work than workers in the Frugal Four countries. In 2018, the average Greek worker worked close to 2000 hours, while the Danish, German and Dutch worked the least out of all EU Member States at only 1382, 1390, and 1431 hours per year, respectively. The average full-time employee in the European South, had a longer work week by 2 hours in 2005 and 2.5 hours in 2018 as compared to a full-time worker in the European North. Although this may not seem like much, it amounts to an extra working day every single month. When factoring in part-time work, the regional difference in hours worked grows for German and Dutch workers. To imply that the Southern economies would fare better if they were as laborious as their Northern counterparts is, therefore, unfounded.

Retirement Policy and Age Thresholds

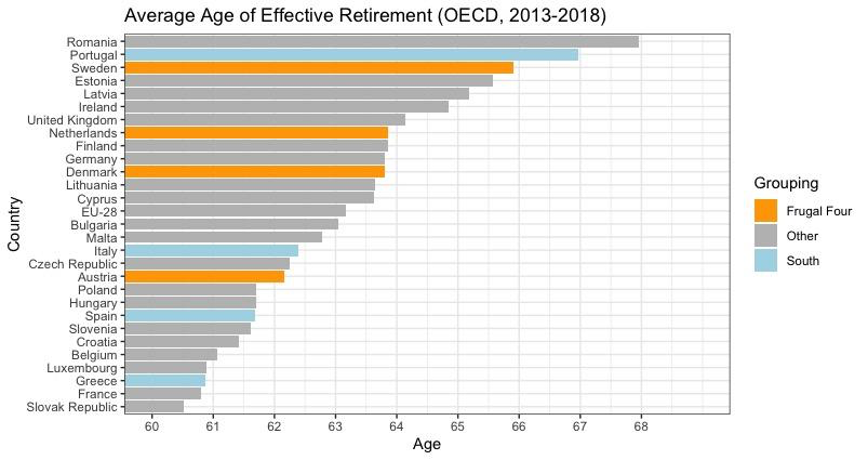

Another key topic in the Frugal Four’s narrative of Southern laziness is retirement age. Data from the OECD on withdrawal from the labor market shows that, with the exception of Portugal, the Southern Member States tended to have a lower average age of effective retirement than the Frugal Four. The average age of effective retirement is measured by recording labour market withdrawal by employees over the age of 40 rather than official retirement per se. This measure is somewhat circumspect as retirement is not the sole cause of labour market exit. A high unemployment rate would similarly result in a lower age of effective retirement. It is also well known that the southern economies experienced significant employment difficulties between 2013-2018.

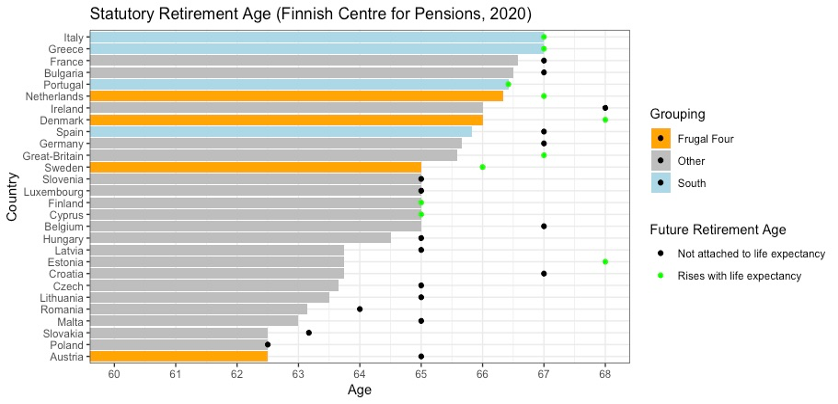

A different picture is painted when examining retirement policies of Member States. In response to ageing demographics and rising life expectancies, most Member States have decided to increase their retirement age. In the graph below, the bars depict the statutory retirement age for each member state as of 2020. These are the earliest ages at which a person can access a publicly provided pension without penalties for early retirement. The points indicate the retirement age that a state intends to move towards (to be reached at different points in time for each country, from 2021 in Greece to 2033 in Austria). The green points indicate whether the country has pegged their retirement age to increases with average life expectancy.

A different picture is painted when examining retirement policies of Member States. In response to ageing demographics and rising life expectancies, most Member States have decided to increase their retirement age. In the graph below, the bars depict the statutory retirement age for each member state as of 2020. These are the earliest ages at which a person can access a publicly provided pension without penalties for early retirement. The points indicate the retirement age that a state intends to move towards (to be reached at different points in time for each country, from 2021 in Greece to 2033 in Austria). The green points indicate whether the country has pegged their retirement age to increases with average life expectancy.

This data complicates the story around retirement ages in Southern Europe. In fact, the Southern states have among the highest European statutory retirement ages and have all set out to increase their retirement ages in the future.[1] All except Spain have tied their future statutory retirement age to life expectancy. On the other side of the continent, the Frugal Four have also set targets to increase their retirement ages and tie them to life expectancy. A notable outlier is Austria, where the statutory retirement age for men is 65, while the statutory retirement age for women is 60, and where only the age for women is set to increase. Although the effective age of retirement was significant lower between 2013 and 2018, the data on statutory retirement age lead us to believe that the Southern states have in fact set out to reform.

This data complicates the story around retirement ages in Southern Europe. In fact, the Southern states have among the highest European statutory retirement ages and have all set out to increase their retirement ages in the future.[1] All except Spain have tied their future statutory retirement age to life expectancy. On the other side of the continent, the Frugal Four have also set targets to increase their retirement ages and tie them to life expectancy. A notable outlier is Austria, where the statutory retirement age for men is 65, while the statutory retirement age for women is 60, and where only the age for women is set to increase. Although the effective age of retirement was significant lower between 2013 and 2018, the data on statutory retirement age lead us to believe that the Southern states have in fact set out to reform.

The Public Finance Critique

Moving from labour market criticisms to public finance criticisms there is a clear implication in the Northern demand for loans contingent on reforms that Southern states cannot manage their own economies. Specifically, this fiscal irresponsibility narrative indicates that they cannot balance their books because they spend too much and have the wrong priorities.

Expenditure

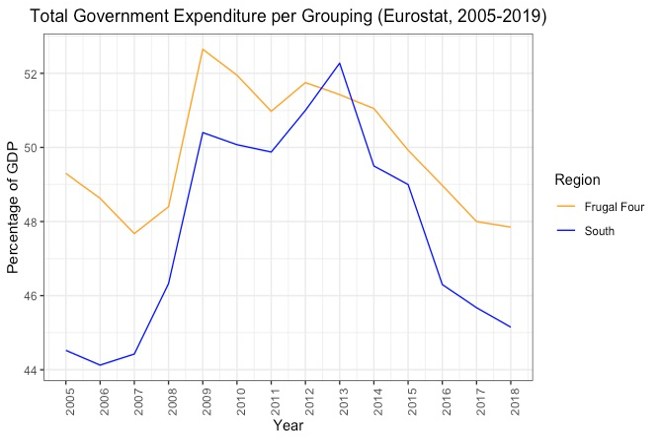

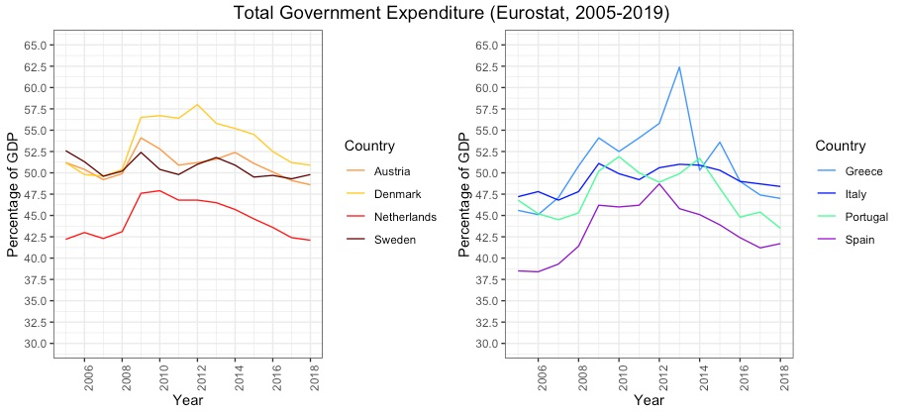

When studying total government expenditure relative to GDP over the past fifteen years we see that, ironically, those who have dubbed themselves frugal seem to be most liberal in their government expenses. The Frugal Four average annual government expenditure is consistently higher than that of the Southern Four, with the exception of 2013. When splitting these averages into individual country trends, we find that the Southern peak in 2013 is caused solely by Greece’s experience during the eurozone crisis. Within the Frugal Four, we find that, hidden by the average, the Netherlands is the only country that, true to its image, is more frugal than the Southern states. Excessive expenditure appears to be an unfounded accusation against the South and not a reasonable explanation for current economic difficulties.

When studying total government expenditure relative to GDP over the past fifteen years we see that, ironically, those who have dubbed themselves frugal seem to be most liberal in their government expenses. The Frugal Four average annual government expenditure is consistently higher than that of the Southern Four, with the exception of 2013. When splitting these averages into individual country trends, we find that the Southern peak in 2013 is caused solely by Greece’s experience during the eurozone crisis. Within the Frugal Four, we find that, hidden by the average, the Netherlands is the only country that, true to its image, is more frugal than the Southern states. Excessive expenditure appears to be an unfounded accusation against the South and not a reasonable explanation for current economic difficulties.

Revenue

Revenue

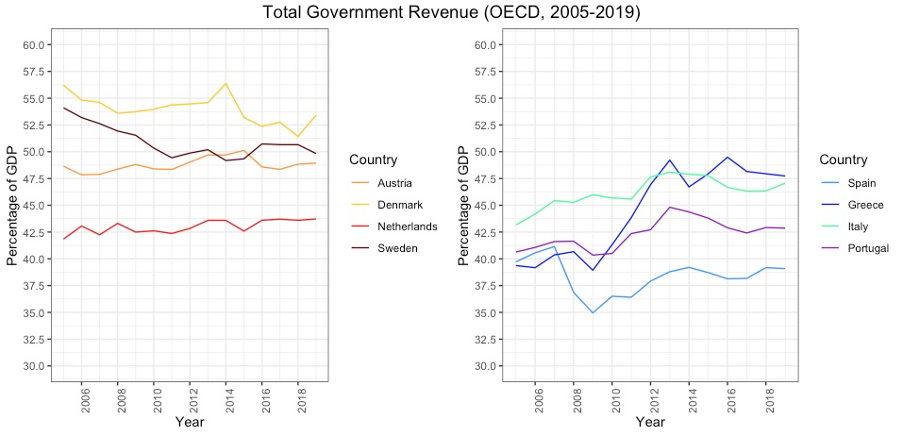

What we cannot overlook, however, is that the higher spending in the Frugal Four is accompanied by a much higher government revenue. Whereas Denmark has consistently raised over 50% of its GDP in government revenue, Spain remains below 40%. These are the two extremes of comparison, but they show that the issue in the South may be more about how much money comes in rather than how much flows out.

Spending by Policy Sector

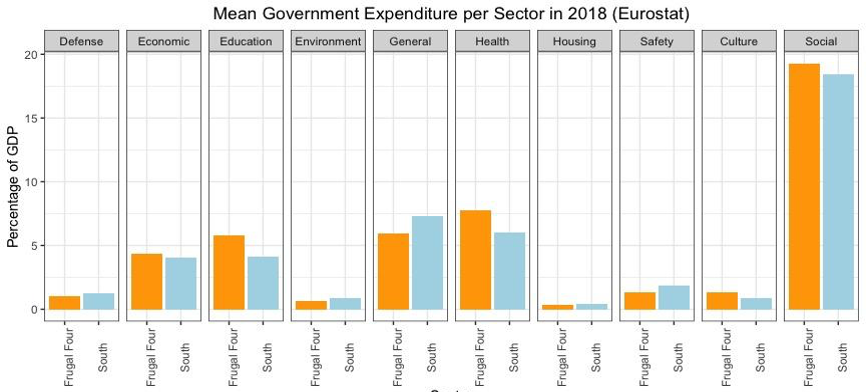

Fiscal irresponsibility is not only an accusation as to how much is spent, but also as to how funds are spent. In the Frugal Four perpetuated myth, the Southern states spend irresponsibly on, for instance, overly generous social measures. Dividing government spending into sectors shows, however, that it is the Frugal Four who spend more on social protection policies and education. In fact, they spend more in almost every sector, with a few notable exceptions. The only charge that might be laid against the South in the face of the COVID-19 crisis is that they might have actually under-spent in the health sector, as compared to the Frugal Four.

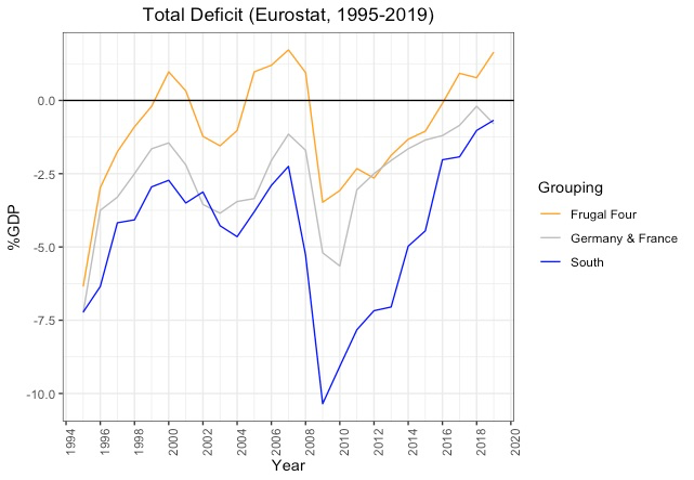

Deficits

When examining the differences between total revenue and expenditure of the total public sector (i.e. deficits and surpluses), the frugal image of the Northern states is undermined. At the same time, their accusation of Southern mismanagement seems to find grounding.

The Frugal Four bloc on average has run an unweighted surplus during 9 out of the last 25 years, while the Southern states have been unable to run one in aggregate as a bloc during that time (although they have on occasion run surpluses individually). The figures for individual countries (not included here) demonstrate the differing effect of the financial and eurozone crises on the public finances of Northern and Southern states. The Netherlands’ surplus shrank from 0.1% in 2006 to a -5.3% deficit by 2010, while Spain’s 2.1% surplus plummeted to a -12.8% deficit by 2012. Except for Italy whose deficit peaked at -5.1% during the eurozone crisis, the southern economies reached double digit deficits.

Primary Deficits

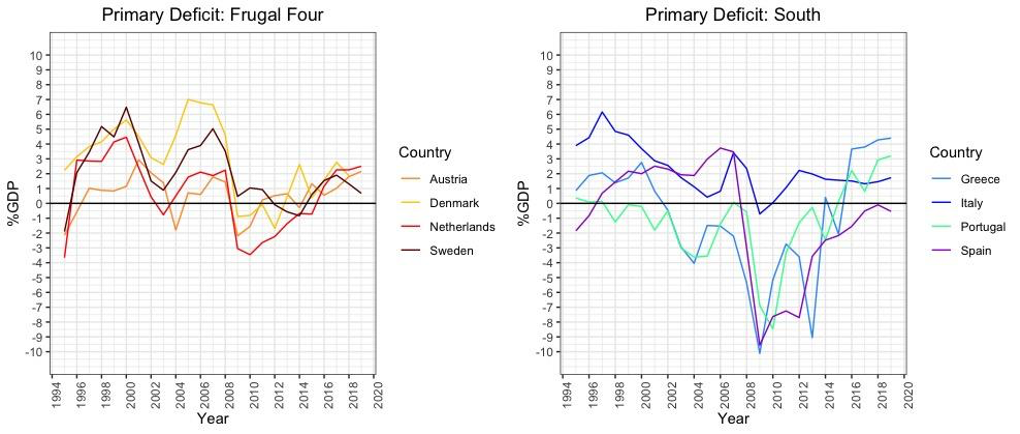

Yet, this headline financial position obscures as much as it reveals. A much more telling figure is the primary deficit, which measures the difference between total revenue and expenditure, excluding interest payments. By excluding debt, the primary deficit tells a more complicated and intriguing story of public finances and this is where the collective story of the South may unravel.

Italy shows itself to be a bona fide member of the frugal four, as it has run a primary surplus for 24 out 25 years from 1995 to 2019. This is better than any Northern economy (including Germany). Spain, on the other hand, has increasingly grown their significant primary budget surpluses since 1995 and reached 3.7% of GDP by 2006 only to be devastated by the financial crisis.

Portugal had been running modest primary surpluses and deficits until the early 2000s when recessionary cycles disrupted their primary budget balance until a 2015 surplus. Greece is a similar story where significant surpluses also fall into a pattern of deficits by recession but, even under the supposedly disastrous Syriza government, they return to balance by 2016.

This counterintuitive data reveals the effect of the intervening variable in the previous deficit statistics and the cost of debt-servicing.

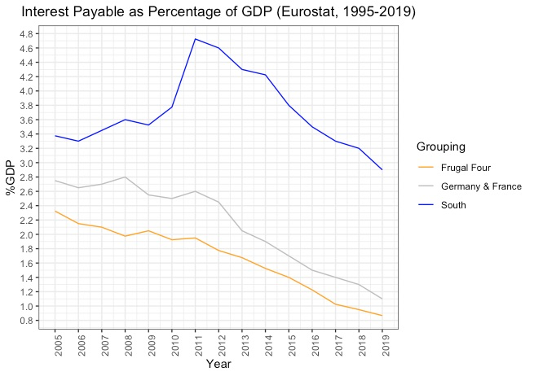

Debt-servicing

The gap between the total and primary surplus/deficit is due to the interest payments of each state on outstanding loans, known as interest payable. Although there is a long-term decline in the interest rate of public debt paid across the eurozone, there remains a significant gap in the burden of servicing each state’s debt load.

As seen below, there is substantial regional variation in the costs of servicing public debt. Southern states pay a much larger share of their national income towards servicing existing debts. In order to then run a total surplus (and pay these debts back), an average Southern state needs to run a primary surplus of 3% of GDP. Between 1995 and 2019, the Frugal Four only managed this surplus rate 23 times (18.5% of the time) and Southern states 14 times (11.2% of the time)

A higher debt naturally means more of your public funds must go to service this debt, but this is also a function of the different costs of borrowing.

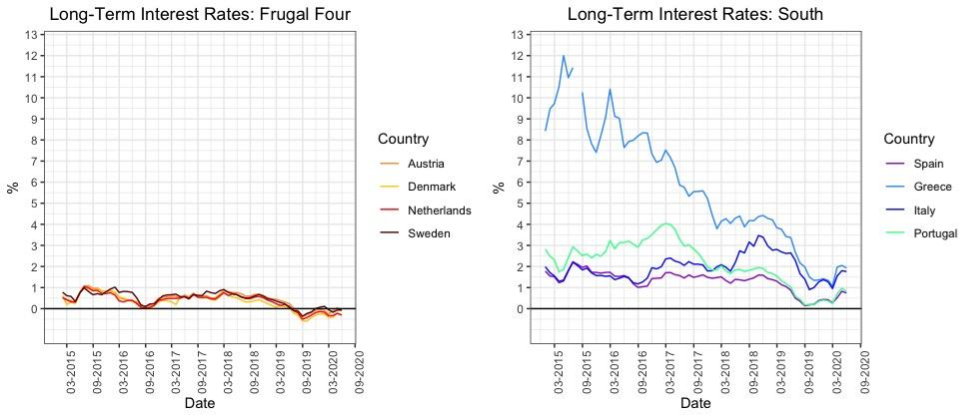

Cost of Borrowing

Eurostat’s long-term interest rate data depicts the bond yields of each state’s debt, as measured in a 10-year bond. This cost of borrowing statistic shows the differential between North and South borrowing costs and the ability to invest. The gap has narrowed, but this phenomenon relies on the European Central Bank to intervene to ease market volatility and suppress the risk premium paid by Southern economies. While the Frugal Four’s bonds have sunk to a negative interest rate, Southern States looking to make similar spending decisions will have to pay a few percentage points more. During COVID-19, as states mobilize billions to keep businesses solvent and households above the poverty line, investment is essential, but each government will be burdened differently.

Conclusion

The differences in debt servicing costs and long-term interest rates will perpetually leave the Southern states at a competitive disadvantage to Northern states who, at a lower interest rate, can more easily finance their debts. The logic of coronabonds is to “Europeanise” the interest rate each state borrows at in order to finance much-needed investment and in the future refinance existing debt onto a lower interest track.

The Frugal Four narrative of fiscal irresponsibility overlooks the fact that Southern states spend less, work more, and are reforming their retirement laws. Their stance in the negotiations has directly opposed the logic behind coronabonds and risks perpetuating the structural imbalance caused by heavy debt loads in the Southern economies. No amount of austerity and hand wringing will resolve this imbalance. In insisting on loans and reforms, the Frugal Four might cause the Southern states to be less, not more, able to ‘solve it by themselves next time’.

[1] Italy’s ‘quota cento’ policy temporarily (until 2021) makes it easier to retire from age 62 with 38 years of contributions.

[i] European debt is not without precedent as the European Union has $52bn in bonds currently outstanding, but the idea remains a highly contentious strategy to revive the Single Market.