COVID-19 and the ECB: How to Manage the Economic Contagion?

9 June, 2020

Two weeks ago, we posted a detailed analysis of the coronavirus’ economic impact in which we demonstrated that the pandemic has caused a major exogenous supply-demand shock. This discussion included an exploration of whether the European Central Bank (ECB) should intervene. Concluding that the COVID-19 crisis and resulting economic contagion represent a clear and serious threat to both price stability (the ECB’s primary objective) and financial stability more broadly, we argued that monetary interventions are essential to mitigating the pandemic’s negative socio-economic consequences and aiding recovery. Consequently, the ECB should seek to stabilize the pandemic’s economic effects. As we enter the worst economic downturn since the Great Depression, failing to act could have devastating consequences.

However, whether or not the ECB should intervene is not the only aspect to this debate. What form such intervention(s) should take is another central component. This discourse has intensified in the last month following the German Constitutional Court’s judgement questioning the legality of the ECB’s original quantitative easing program. While the legal framework of the ECB’s actions is certainly an important part of this conversation, it is also imperative to conduct a deeper examination of the macroeconomic implications of the institution’s policies. This expands beyond whether the ECB should intervene to encompass an analysis of the consequences of the various interventions at the bank’s disposal. These are the crucial issues this article will explore.

How Can the ECB Respond? What are the Consequences of Different Types of Interventions?

The European System of Central Bank (ESCB) consists of the ECB and the national central banks of the Euro area. Its primary mandate is to maintain price stability, as established by Article 127 (1) of the Treaty on the Function of the European Union (TFEU). Without prejudice to this objective, the ESCB shall also “support the general economic policies in the Union with a view to contributing to the achievement of the objectives of the Union,” which include inter alia economic growth and job creation. To accomplish these goals, the ECB carries out a number of tasks including: setting the interest rates at which it lends to commercial banks in the Eurozone, authorizing production of euro banknotes by Eurozone countries, managing the Eurozone’s foreign currency reserves, buying or selling currencies to balance exchange rates, ensuring financial markets and institutions are well supervised by national authorities, ensuring the safety/soundness of the European banking system, and monitoring price trends and assessing risk to price stability.

Ultimately, these actions can affect interest rates, the amount of credit, and the money supply—all of which can impact financial markets, inflation, and employment levels. The ESCB’s operational framework comprises of various instruments (i.e., open market operations, standing facilities, minimum reserve requirements for credit institutions). Since 2009, however, the ECB has implemented several non-standard monetary policy measures. These instruments and measures illustrate the various interventions at the ECB’s disposal. We will examine three of these interventions, specifically lowering interest rates, quantitative easing, and dual interest rates.

Lowering Interest Rates

Central banks can react to a crisis, like a pandemic, by lowering interest rates which lowers borrowing costs. This intervention can (a) help alleviate fears that debtors will not be able to service their existing debt, (b) induce individuals and firms to increase borrowing and spending, and (c) make it cheaper for governments to borrow money to pay for a disaster response. In doing so, it could, ultimately, increase aggregate demand. However, in both the 2008-2009 financial crisis and the current COVID-19 pandemic, lower interest rates have not been enough of an incentive to increase aggregate demand to desired levels. In theory, if the monetary stimulus is strong enough, full employment may be restored though most likely at the cost of overshooting inflation targets. Monetary easing can also reverse a supply-demand doom loop as higher demand encourages businesses to increase their investments, which in turn sustains consumers’ expectations of future income and leads to a further rise in demand.

Historically, lowering interest rates has been the primary tool utilized by central banks, like the ECB, to affect financing conditions within the economy. Perhaps unsurprisingly, it has been overused. The Governing Council of the ECB sets three key interest rates: the interest rate on the main refinancing operations, the rate on the deposit facility, and the rate on the marginal lending facility. As of September 18, 2019, these rates were 0.00%, -0.50%, and 0.25% respectively. The rates currently remain unchanged. These numbers hint at another reality—there are limits to such conventional monetary policy, specifically the zero-lower bound (ZLB). When interest rates are close to zero, reducing them further will have little impact. Furthermore, crossing the ZLB into negative interest rates depletes the income lenders receive by making them pay to keep money at the central bank (rather than earn interest on it) and damages bank profitability—both of which can cause other serious consequences. While a recent controversial paper by the ECB attests that the bank’s negative deposit rate has had a “broadly neutral” impact on bank profitability (as “their negative effect on net interest income has been offset by a positive effect on borrower creditworthiness”), it did, however, acknowledge that such rates risk becoming counterproductive the longer they last.

Moreover, there are other consequences to this type of intervention. Lowering interest rates can encourage individuals and companies to take on new and/or more debt. If these agents take on too much debt, they may be unable to service it once interest rates (most of which are variable) rise in the future. We witnessed a similar situation unfold during the housing crisis. Specifically, low interest rates and easy mortgages acted as incentives for individuals (including sub-prime lenders) to take on too much debt. When large numbers of people could no longer pay these mortgages, this led to a high default rate. While during the COVID-19 crisis there is less concern with individuals repeating these actions, it is possible that companies and governments will take on too much debt. If this does occur and governments default on their obligations, there are no international courts to demand that they do so, although there are reputational effects (e.g., Argentina, Lebanon).

Quantitative Easing

When central banks do approach the ZLB, they have to start employing other unconventional monetary policies, such as quantitative easing (QE). An expansionary monetary policy in which central banks purchase large quantities of longer-term assets (e.g., government debt, corporate debt, equities), QE increases the monetary base while decreasing the supply of these longer-term assets. In theory, this places upward pressure on these assets’ prices while decreasing their yield. Ultimately, the intention is for these purchases to add money into the economy, lower long-term borrowing costs, and support job creation. As there are many different types of QE that use different purchasing facilities, QE may act as a more granular tool within the monetary policy toolbox. For instance, the ECB has adjusted its program to grandfather marketable assets and issuers that met the minimum credit quality requirements for collateral eligibility on April 7, 2020. The ECB could theoretically expand these limits further, although such decisions would heighten the risk of moral hazard.

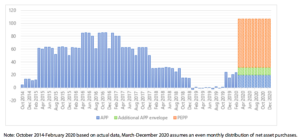

As mentioned previously, the ECB has employed several non-standard monetary policy measures in response to the 2008-2009 financial crisis. Since mid-2014, this has included QE under the name of the Asset Purchase Program (APP). A set of QE packages, the APP consists of a corporate sector purchase program (CSPP), public sector purchase program (PSPP), asset-backed securities purchase program (ABSPP), and third covered bond purchase program (CBPP3). These programs were employed to various degrees between October 2014 and December 2018 (Figure 1). On September 12, 2019, the ECB announced it had decided to restart net purchases on November 1, 2019 under the APP at a monthly pace of €20 billion. On March 12, 2020, the ECB decided to increase the program by adding an additional envelop of €120 billion to be used by the end of 2020. The decision formed part of the institution’s response to the coronavirus pandemic.

Figure 1: ESCB net asset purchases by month (EUR billion)

In the wake of the crisis, the ECB has initiated a second QE program known as the Pandemic Emergency Purchase Program (PEPP). A temporary asset purchase program of private and public sector securities, the PEPP has an overall envelope of €750 billion and includes all asset categories eligible under the APP. It will be terminated once the Governing Council determines the COVID-19 crisis phase is over, but not before the end of 2020. Moreover, the Governing Council has expressed its readiness to increase the size and adjust the composition of the program if necessary. Due to this and the ECB’s other QE programs over the years, the ECB’s balance sheet has increased substantially.

As QE is still a relatively new and controversial policy with limited empirical evidence, its effectiveness is still up for debate. Proponents maintain it combats deflation and allows central banks to take more extreme measures, or in other words “do whatever it takes.” However, empirical assessments of QE programs are globally below expectations. For example, Japan’s QE program in the early 2000s to fight deflation produced mediocre results. And the significant impact QE measures have typically had on sovereign and private yields have been relatively short-lived. Other critics cite the length of time it takes to see results and the dangers associated with printing trillions of dollars.

In the case of the ECB, these critiques extend to a question of whether the bank’s QE policy extends beyond its primary mandate. Concerns also cite Article 123 (TFEU), which states that the ECB must not finance Eurozone governments. This question has most recently come up in the wake of the German Constitutional Court’s May 5, 2020 decision in which the court stated that the ECB’s original asset purchase program did not respect the principle of proportionality. Or more specifically, the concept that the EU’s actions must refrain from going beyond what is necessary to achieve the objectives of the treaties. While the ECB should be able meet the conditions set by the Court and illustrate it acted proportionately, the decision has incited contention with some concerned that it not only threatens the PEPP, but further chips away at the EU’s stability.

Furthermore, in theory increasing the money supply can lead to high inflation. Although in the case of recent uses of QE this has yet to be seen, inflation is currently growing in Europe but has not yet hit the target rate of 2%. In addition, as previously mentioned, exceedingly low interest rates can encourage abnormal levels of consumer and business debt. Lastly, the effectiveness of QE programs can be constrained when the weakness of credit is the result of both supply and demand factors—as is the case both in the Eurozone and the coronavirus crisis. Enhancing the effectiveness of QE requires employing additional complementary policy measures that facilitate sustainable economic risk taking, contain resulting financial excesses, and look towards restoring balance sheet health in the future.

Dual Interest Rates

Lastly, another policy approach the ECB could explore further amidst the COVID-19 pandemic is dual interest rates, particularly raising interest rates on deposits while cutting interest rates on loans. Historical evidence, including from the Chinese banking system in the 1980s and early 1990s, indicate that this approach would lead to a rise in demand. The ECB has adopted this method of independently affecting lending rates through its targeted longer-term refinancing operation (TLTRO). Through this program, the ECB can lend to commercial banks at negative interest rates on the condition that the money is eventually lent to companies (rather than mortgages or buying government debt).

While at -0.5% the current three-year TLTROs are only a marginal improvement on available market-based funding, experimenting with a more aggressive option (e.g., a 10-year loan at -1 or -2%) could be something to consider during a pandemic. The main concerns with dual interest rates are that (a) it could impact the central bank’s balance sheet and even, theoretically, lead to a decline in its net interest income and (b) banks could game the system. A decline in net interest income would, for instance, occur if the interest rate at which targeted loans are made to banks falls below the interest rate the central bank earns on reserves.

Concluding Remarks

Analyzing three of the specific interventions at the ECB’s disposal, we see that no option is perfect. Each has various consequences, some more severe than others. Hence, while the ECB should seek to stabilize and protect the economy, they should not deploy unlimited means to do so. Rather, an effective course of action needs to balance the short-term pain of the coronavirus’ economic contagion with the long-term implications of such measures. Furthermore, it is important to emphasize that no matter which instruments the ECB chooses to utilize, they must consider how these actions will interact with fiscal policy and the broader economic goals of the European Union. Such interactions may alter the impact of the original policy. No monetary intervention exists in isolation and some interventions are more appropriate for certain contexts.